Apr 01, 2025

Strategy Bulletin Vol.376

The Contrasting Change of Balance of Payments between the U.S. and China

~ The Real Cause of the Trump Administration's Major Shift in Global Strategy~

Who would have thought the U.S. would be cornered to this point! The U.S. current account deficit is rapidly increasing, while China's surplus is rapidly increasing. A major change in the balance of payments between the U.S. and China will inevitably change the balance of power. The U.S. has been forced to drastically adjust its strategy toward China. The Trump administration's wild attempts to reorganize the international order are rooted in this sense of crisis. If nothing is done, U.S. hegemony is in jeopardy. We should assume that the Trump administration's new trade strategy is based on this sense of crisis.

(1) Markets at the mercy of policy uncertainty

U.S. stocks under correction; the pretext is policy uncertainty

As the Trump administration's policy uncertainty has peaked, the stock market has indeed become increasingly turbulent: the SP500 index fell 10% from its all-time high of 6144 points on February 19 to its all-time low of 5488 points on March 31, giving back all the gains it has made since Trump's election. The era of unipolar traction in U.S. stock prices appears to be over.

This stock price adjustment can be attributed to a combination of three factors: 1) Trump's policy shock and uncertainty, 2) recession and stagflation fears, and 3) the autonomous adjustment of the stock market, which had been soaring.

Certainly, policy uncertainty is on the rise. The international order is in turmoil due to tariff hikes and other measures, the U.S. is increasingly at odds with its ally Canada and the EU, and the administration's policy intentions have become completely unreadable due to a series of unconventional policies, such as rushing to end the war in Ukraine and siding with Vladimir Putin. However, the actual economic situation is solid, and the overvaluation of stock prices has been wiped out. It is conceivable that concerns about the Trump administration's policies will ease in the future.

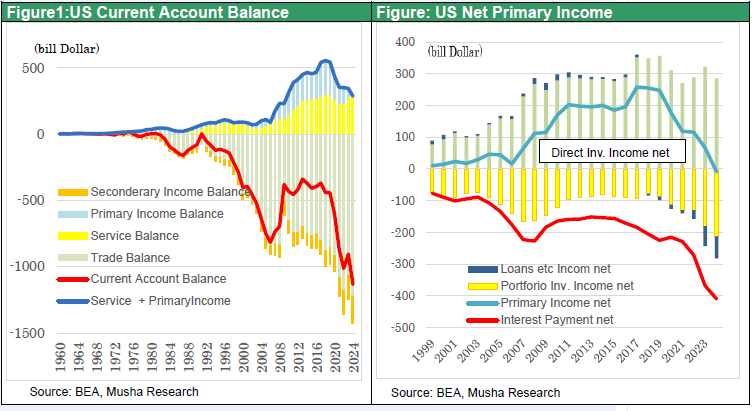

Figure 1: U.S. Current Account Balance and Breakdown of Rapidly Deteriorating Balance

Figure 2: U.S. Income Balance and Breakdown

If the aims of the Trump administration's economic policies are clarified and there is a growing belief that they will work, there is a good chance that the policies will have a positive effect on stock prices.

Trump policies such as tariffs may turn from a cause for concern to a positive factor

Now may be the time to invest. The reasons are: 1) Mr. Trump is essentially a pro-market administration; 2) There is a possibility that the negative policy factors (tariffs, restructuring of government employees, deteriorating consumer sentiment) that are currently in the forefront will be replaced by positive factors (tax cuts, deregulation, domestic investment (= domestic production)); and 3) The current slowdown is a temporary one due to the rush to imports, and there is still much room for interest rate cuts, so the economy will not collapse. The high-pressure economic framework is expected to continue.

(2) Noticeable deterioration in the U.S. balance of payments and the difficulty of continuing support for Ukraine

Expanding Trade deficit, rising interest expenses, and support for Ukraine

The U.S. current account deficit continues to widen on the vine. As seen in Chart 1, the pace of increase is gaining momentum with a 2.5-fold increase from $441.7 billion in 2019, just before the Corona pandemic, to $1.133 trillion in 2024. The trade deficit has not slowed down, reflecting strong consumption. In addition, the primary income balance, which had made large surpluses along with digital services, has fallen into the red for the first time. Rising interest rates have led to a substantial increase in foreign interest expenses, eating up all the substantial earnings of U.S. companies from their overseas operations (see Chart 2). Added to this was a sharp increase in the secondary income balance deficit due to support for Ukraine. According to Germany's Kiel Institute for the World Economy, the cumulative amount of military, humanitarian, and financial aid totaled 267 billion euros (about 42 trillion yen) by December 2012. U.S. assistance amounted to €114 billion, accounting for 40% of the total.

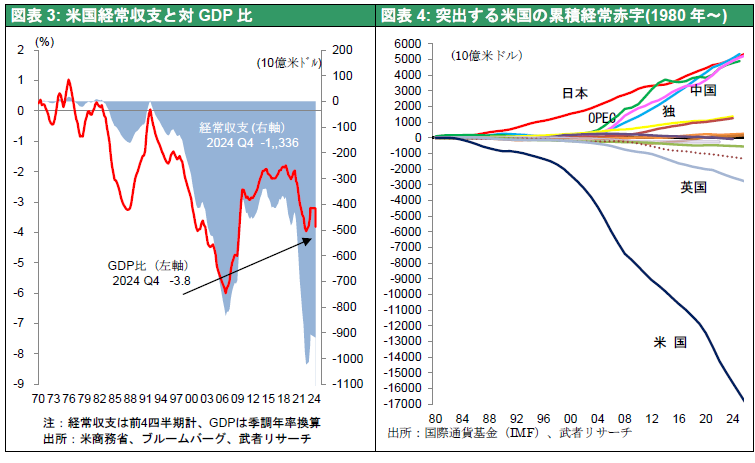

Figure 3: U.S. Current Account Balance and Ratio to GDP

Figure 4: Accumulated U.S. Current Account Deficit (1980-)

If this trend continues, it will eventually become unsustainable

Is this rapid increase in the deficit at an unsustainable level? Chart 3 shows that the deterioration is as steep as that between 2000 and 2006, but not as steep as the worst period (5.8% in 2006), at 3.5% of GDP (2024). However, unlike then, as shown in Chart 4, the accumulated foreign debt of the U.S. has increased significantly, from $5.97 trillion in 2006 to over $16.27 trillion at the end of 2024, almost triple the 2006 level. Therefore, if interest rates rise sharply from this point, interest payment expenses will increase sharply, causing the dollar to weaken, interest rates to rise (bonds to weaken), and stock prices to fall, which could lead to a major recession. Such a major recession could wreak catastrophic havoc on the global economy and geopolitics, given the remarkable rise of China, which will be discussed later in this report.

Why Tariffs Emerge as Optimal Policy

How can the U.S. stop the current account deficit from expanding while avoiding a recession? The privilege allowed under the US monopoly of accumulating foreign debt on the back of a strong dollar and continuing elevated levels of consumption through substantial imports may no longer be sustainable.

The response currently left as an option would be to substitute imports with domestic production while accelerating the increase in digital revenues, which is a U.S. strength. Aiming to reduce the foreign trade deficit and increase employment by promoting domestic manufacturing while continuing to expand consumption is not a sure thing, but it is a policy with good prospects for success. How can imports be substituted for domestic production? The side effects of a weaker dollar are too great, such as inflation (i.e., lower real income in the U.S.), which will suppress consumption, and higher interest rates, which will reverse the flow of funds into the U.S. The only remaining policy options are tariffs and import restrictions, which are deviations from WTO rules. (Note)

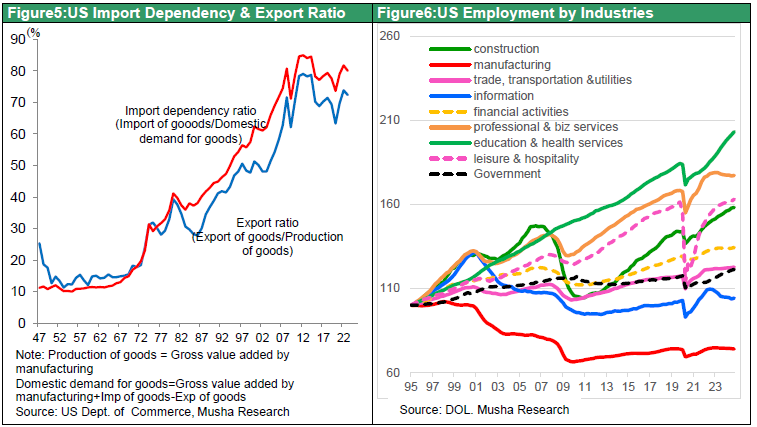

As shown in Figures 5 and 6, comparing the period before China joined the WTO to today, the level of U.S. goods imports rose from 50% to 80%, and manufacturing employment was lost by 30%.

Figure 5: U.S. Goods Import Dependence and Export Ratio

Figure 6: U.S. Employment Change by Sector

(Note) Incidentally, a bold policy idea called the Mar-a-Lago Accord was proposed from within the Trump administration (by CEA Chairman Stephen Milan), which would also justify the deviation from WTO rules in the form of tariffs and import restrictions. The Mar-a-Lago Accord is a policy idea to bring manufacturing back to the U.S. It is based on the following three conditions: 1) countries that benefit from the U.S. defense capability must induce the depreciation of the dollar through coordinated intervention, 2) countries that benefit from the U.S. defense capability must switch their U.S. Treasury holdings to 100-year bonds in order to limit the rise in interest rates, and 3) If they do not agree to the agreement, they will be subject to tariffs and excluded from the benefits of the U.S. defense force. Countries that receive benefits from the U.S., such as 1) access to the U.S. market and 2) protection of defense capabilities, should pay a reasonable cost. There is basic recognition that if they do not, the current system will collapse.

Why target Canada, Mexico, the EU, and Japan for tariffs instead of China?

Musha Research had believed that the main thrust of the Trump tariffs, which came out of nowhere, was to curb China, but this was not perfectly correct. If the U.S. does not have the capacity to substitute production (of Chinese imports), suppressing imports from China will have negligible effect on the quickest way to increase domestic production. Rather, curbing imports from Mexico, Canada, the EU, Japan, and other countries will directly lead to an increase in U.S. production.

In this light, it is not surprising that automobiles, which have a sufficient production base in the U.S., are the target of the tariff hikes. Hyundai Motor Company's announcement of a massive $21 billion (¥3 trillion) investment in the U.S. can be seen as a sign that the effects of the Trump tariffs are beginning to take effect.

Given the balance of payments situation in the U.S., it is not surprising that the Trump administration is reluctant to continue its support for Ukraine.

(3) Dramatic Improvement in China's Balance of Trade and Continued Leap in Industrial Power

China's trade surplus has increased 2.8 times in the six years since sanctions began

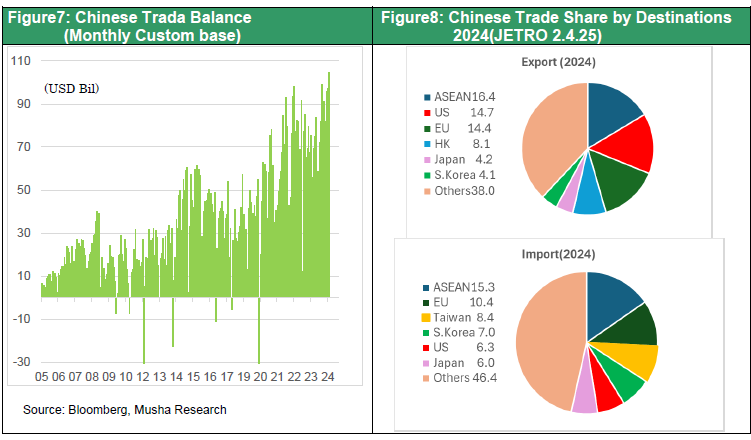

In contrast, China's trade surplus has continued to increase in 2024, exports totaled $3,577.2 billion (up 5.9% from the previous year), imports totaled $2,585 billion (up 1.1%), and the trade surplus totaled $992.2 billion (up 20.5%). China's trade surplus was $351 billion in 2018, the year the U.S.-China conflict erupted, so it has increased 2.8-fold over the past six years (Figure 7). By partner country, there has been a noticeable increase in exports to ASEAN and emerging economies, as the country has moved away from its former dependence on Europe and the United States. According to the JETRO Business Report (February 4, 2025), exports of ships were $43.4 billion (up 57.3% from the previous year) and integrated circuits $159.5 billion (up 17.4%). (+17.4%), and automobiles $117.4 billion (+15.5%).

Figure 7: China's Trade Balance (Monthly Customs Clearance)

Figure 8: China's Import/Export Ratio by Country, 2024 (JETRO Business Report 2.4.25)

Industrial power with a global share of just under 40%, three times that of the U.S

China's presence in global manufacturing increased significantly in the six years following the imposition of sanctions against China in 2018. With 17% of the world's population, China has become the dominant industrial power. China's share of global manufacturing rose to almost 40%, making it three times as productive as the U.S. and five times as powerful as Japan. Not only does it have an overwhelming share of the heavy industry, with a 50% share of crude steel production (2024) and a 70% share of shipbuilding orders (2023), but it has also conquered the world in advanced green energy. It has secured a dominant global share of 60-90% in solar power generation, wind power generation equipment, drones, EVs, and batteries. In addition, it has secured the rights to rare metals used in batteries and other products in various resource-rich countries and has captured most of the world market for most rare metal refining.

China is also closing in on semiconductors

China is expected to significantly increase its production share of semiconductors, the only area where it has lagged, through major investments in existing (legacy) areas that were not subject to export restrictions. China's share of global purchases of semiconductor production equipment in 2023-2024 reached 40%, and Knometa Research (successor to IC Insights) forecasts that China's share of the global semiconductor market in 2026 (on a wafer input basis) will be 22.3%, the largest share in the world. Of course, China's market share in value terms will be much lower than that due to its lack of cutting-edge, high-priced products. However, China is significantly increasing its capacity in analog semiconductors, power semiconductors, DRAM, and other memory products, and there is a strong possibility that it will intensify its low-cost export offensive. As in the case of solar panels, China's share of the legacy semiconductor market may increase significantly. As U.S. Secretary of State Marco Rubio has acknowledged, the “China Manufacturing 2025” (to achieve a leading position in key technologies and become a manufacturing powerhouse) launched in 2015 is seen as having been achieved.

(4) Sanctions against China since 2018, which were a huge failure, and predictions of China's decline due to sanctions were off

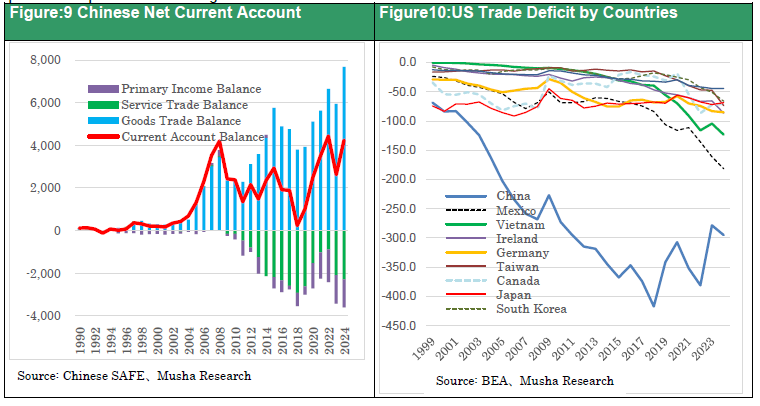

As seen in Chart 9, in 2018, when the U.S.-China confrontation erupted, China's current account balance had fallen to almost zero at $24.1 billion due to a decline in the trade surplus and a sharp increase in the services deficit, including the travel balance. It was at this juncture that sanctions such as tariff hikes and restrictions on exports of high-technology products to China were imposed, and there were even fears that China would be plunged into serious foreign currency instability. Musha Research also published “Strategy Bulletin No. 205, Trade War Mid-Term Summary, U.S. succeeds and China retreats” (2018 / 8 / 21) https://www.musha.co.jp/short_comment/detail/205や “Strategy Bulletin No. 207, Japan will clearly be a beneficiary as the US-China trade war continues ,” (2018 / 9 / 5 ) https://www.musha.co.jp/short_comment/detail/207, but this outlook has gone very wrong.

Even under sanctions against China, dollar supply from the U.S. continued at a pace of $400 billion per year

Sanctions against China since 2018 have had no effect at all. As seen in Chart 10, the U.S. trade deficit with China declined, but deficits with Mexico, Vietnam, and other countries rose sharply, a significant portion of which may have been due to the localization of Chinese firms and the bypassing of exports by U.S. firms that had outsourced production in China. China was able to compensate for the decline in exports to the U.S. to a considerable extent by increasing exports of components and other goods to ASEAN.

Figure 9: China's Current Account Balance and Its Breakdown

Figure 10: U.S. Trade Deficit by Partner Country

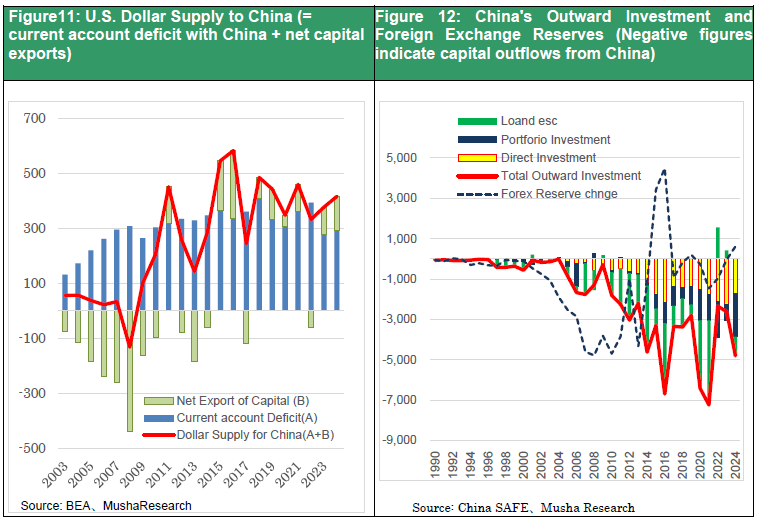

Despite the ongoing sanctions, the massive supply of dollars to China continued. Figure 11 shows the direct dollar supply from the U.S. to China (current account deficit + net capital exports), which has remained at a high pace of $400 billion (¥60 trillion) per year since 2018. Not only did this dollar supply prevent the feared second China shock, but China has also begun to use surplus dollars to enclose the global South. Chart 12 shows the use of dollar funds procured by China, and the high level of outward direct investment, outward investment in securities, and outward loans continues.

A supply chain with China at its core began to form

Until the China shock of 2015, China had been hoarding its external surpluses as foreign exchange reserves and returning the entire amount to the United States in the form of investments in U.S. government bonds. Since 2018, however, China has been accelerating the sale of U.S. Treasuries and deploying the resulting funds and large trade surpluses for global investment. This is a decisive difference in investment stance from Japan, which has continued to return dollars earned from large exports to the US and investment earnings in the US to the US in the form of US government bonds and investments in US companies.

We had viewed the significant sales of U.S. Treasuries by China, which began to become noticeable around 2018, to fill China's foreign currency shortfall, but we appear to have been wrong. It is increasing its presence as an ally of One Belt One Road, BRICS, and the Global South. A global supply chain with China at its core is now being established. The situation points to the fear that the exclusion of China could conversely isolate the West and the United States.

Figure 11: U.S. Dollar Supply to China (= current account deficit with China + net capital exports)

Figure 12: China's Outward Investment and Foreign Exchange Reserves (Negative figures indicate capital outflows from China)

Two Fortunes, a Pandemic, and Benefits of Sanctions Against Russia

Why did China become so powerful? Two fortunate factors. The first was the Corona pandemic. When production in other countries almost came to a halt, China was the only country that was able to operate its plants, and it quickly increased its share of the global market. The supply of masks from China in the wake of the global shortage is a good example of this.

The second fortunate event was Russia's invasion of Ukraine in February 2022. The embargoes imposed by Western countries against Russia resulted in a serious shortage of goods. China seized the opportunity to supply Russia with a great deal of goods. The value of Chinese exports to Russia and China's share of Russian imports rose sharply from $67.2 billion (23% share) in 2021 to $111.4 billion (39%) in 2023 and to $83.2 billion (41% share) in the January-September period of 2024. In addition, the Sino-Russian economic bloc was formed through the purchase of Russian crude oil. It played a decisive role in the continuation of the war in Ukraine (according to JRTRO).

Trends that cannot be stopped by ordinary means

Even without such good fortune, it is highly likely that the trend of China's production capacity expansion would not have stopped even after the sanctions were imposed. This was due to the economic hysteresis effect (past momentum shapes the future), whereby once a trend gains momentum, it is not likely to change half-heartedly. China, where the rule of law does not apply, has hidden policy power, and the vast human network built between the U.S. and China facilitates the outflow of technology, human resources, and technology theft from the U.S. These factors are believed to have had an effect. This is a significant difference from Japan, which easily succumbed to U.S. sanctions and completely lost its industrial competitiveness.

If this is the case, then more stringent tariffs and trade restrictions will be necessary to reduce China's presence in the world.

(5) U.S. strategy toward China has undergone a major shift, with tariffs now at the center of U.S. policy

Deflation, consumption restraint, and excessive savings are intensifying China's domestic economic turmoil.

While China's global presence has grown remarkably as described above, China's domestic economy is becoming increasingly chaotic. The real estate bubble is on the verge of bursting, and further declines are inevitable. Regulations on real estate transactions have curbed supply and artificially restrained price declines, but this has only prolonged the adjustment. Real estate sales continue to decline at a 30% pace, and by 2024 they will have halved from their peak. Real estate investment, which once accounted for 30% of GDP, has also continued to decline by 10% year over year. In addition, the decline in real estate prices has led to a sharp decline in local government sales of real estate use rights, resulting in financial strain. Local government fiscal revenue peaked in 2021 at just over RMB6 trillion (40% of total revenue), but this figure is reported to have been cut in half by 2024.

As a matter of course, the pessimistic view about housing prices has been increasing. To stimulate real estate demand, the government has lowered loan interest rates and down payment ratios, extended loans to real estate agents for the completion of uncompleted properties for which payment has already been received and purchased unsold housing stock and converted it to public housing. However with rising job insecurity and a growing sense of uncertainty about the future of real estate prices, people are forced to cut back on consumption, which is leading to further economic contraction. In China, where social insurance and pensions are underdeveloped, the only thing the average person can rely on is savings.

CPI is at 0% y/y, PPI has been negative since 2023, and the economy is in a deflationary phase. The current Chinese economy is being supported by increased exports of EVs and other advanced technology products, increased capital investment in the so-called “new quality industry,” and a boost in personal consumption due to measures to stimulate demand by the authorities. However, this is not sustainable policy dependence, and there is a possibility that downward pressure on the economy may intensify due to a reactionary decline in the future.

China is approaching 19th century-style imperialism, and the danger of external expansion is increasing

This structure, in which strong investment strengthens oversupply and external competitiveness while stagnant domestic consumption increases excessive savings, is the very danger of imperialism pointed out by Hobson and Lenin (Strategy Bulletin No. 374, “Is Trump an Imperialist?” https://www. musha.co.jp/short_comment/detail/374).

The U.S. Engagement Policy toward China since the beginning of the 21st century has created “a huge imbalance of industrial power without demand (= a monster called China).

How should we deal with China? The neocon approach of pressuring China to change its communist dictatorship is no longer possible. Since neocon leaders such as John Bolton and Mike Pompeo, who oversaw diplomacy and national security in the first Trump administration, were not recruited, the second Trump administration is seen to have turned to the realist side.

Realism of Deterrence and Coexistence with China

If the era of coexistence with China will continue, a strategy to restrain China in the long run will require China containment, like George F Kennan's (George Kennan) policy of containment against the Soviet Union. Kennan dismissed the Soviet Union as a power that 1) fanatically believed that it was desirable to destroy the harmony of American society, crush the American way of life, and drag down its authority in order to ensure its own stability, and 2) unlike the Nazis, did not take risks, and argued for the possibility of coexistence. So, what about China today?

Elbrige Colby, described as a modern-day Kennan, has taken a seat at the center of U.S. military strategy as Under Secretary of Defense. In his book, “Asia's First: A New American Military Strategy,” Colby argues that 1) China is the greatest threat and that all resources should be directed toward Asia, 2) it is necessary to stop China from changing the status quo and using force, such as its advance on Taiwan, and 3) he does not seek regime change in China. He would remind Xi Jinping that the cost of the use of force would be high, and that he must stop the action beforehand, but not push China into a corner and continue to coexist.

It should be clear that Trump's tariff policy relies on the above global perceptions. To revive U.S. manufacturing, allies will have to pay the cost. But to curb dangerous Chinese industrial might, big tariffs and trade restrictions will be essential. During the campaign, Trump went on to say that he would impose a 10% tariff on all imports and that he was considering imposing a 60-100% tariff on China. This may be the drop-off point for Trump tariffs.