Oct 31, 2024

Strategy Bulletin Vol.367

Why are post-election stock prices expected to rise in Japan and the U.S.?

~Full-scale launch of fiscal policy ~

(1) Clear public will: Tax cuts and overcoming deflation to increase household incomes

In the general election for the House of Representatives Oct27, the ruling Liberal Democratic Party (247 to 191 seats) and the Komeito Party (32 to 24 seats) suffered heavy defeats, with both parties losing 72 seats, respectively, falling short of a majority (233). Opposition parties, on the other hand, made particularly remarkable progress, with The Constitutional Democratic Party of Japan(CDP) (98 to 158), Democratic Party For the People (DPP)(7 to 28), the Reiwa Shinsengumi (3 to 9), and two emerging conservative parties (Party of Do It Yourself and Conservative Party of Japan) (1 to 6). This might appear to be a swing in support from conservative to liberal, but this is not the case at all.

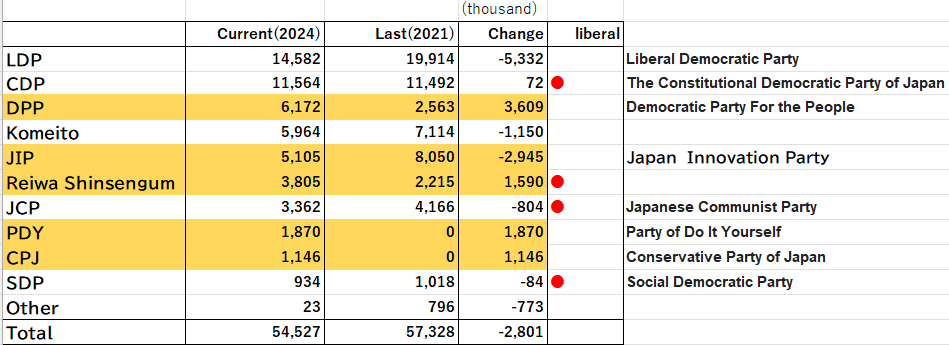

Figure 1: Comparison of the number of votes received by each party in the proportional representation of the House of Representatives election

A comparison of the number of votes received by each party in the proportional representation, which is considered to more accurately represent the will of the people, shows that the LDP lost 5.37 million votes, from 19.91 million to 14.58 million, while the CDP gained only 72,000 votes, from 11.49 million to 11.56 million. All the losses of the LDP went to the DPP (2.56 million to 6.17 million), up 3.61 million votes, and the two emerging conservative parties (0 to 3.01 million), up 3.01 million votes. The policy difference between LDP and DPP and the two emerging conservative parties is their attitude toward tax cuts. DPP advocates a substantial income tax cut, called the elimination of the 1.03-million-yen barrier, while all the conservative opposition parties advocate a cut in the consumption tax.

The same is true between the liberal parties, where there is a huge shift of votes from parties that raise taxes (or are neutral) to parties that cut taxes. Japan Communist Party, which advocates tax hikes on large corporations, lost 800,000 votes (from 4.16 million to 3.36 million), and the Social Democratic Party lost 80,000 votes (from 1.01 million to 930,000), while Reiwa, which is committed to cutting taxes (from 2.21 million to 3.81 million), gained a significant 1.6 million votes. The will of the people, whether conservatives or liberals, was to increase household disposable income by promoting tax reductions.

Takuji Aida, chief economist at Credit Agricole Securities, commented, “In terms of proportional representation, older parties outnumber newer parties when looking at voters in their 50s and older. However, when we look at voters in their 40s through 20s, we find that the newer parties such as DDP、Reiwa, PDY and CPJ outnumber the older parties. Younger voters are more likely to support boosting Japan's economic potential through aggressive fiscal measures and to question the fiscal management that has led to economic stagnation in the past, such as the self-imposed economic sanctions with their emphasis on fiscal soundness.” He stated. Never has the will of the people so clearly indicated its policy demands.

The LDP will continue to work to build a majority by involving the opposition parties, and the axis of this effort will be the policy of tax reductions. In response to the opposition's demand for tax cuts, a barrage of criticism has come from the media and other sources, such as the Nikkei Shimbun's October 15 editorial, “It is irresponsible to give away a hefty sum of money without talking about the source of the revenue. According to the editorial, “A world with interest rates has become a reality, and it is inevitable that the cost of government bonds, which is used to pay principal and interest, will increase. If we easily increase the issue of government bonds, it will be a disaster for the future.” This assertion is false. A world with interest rates is an inflationary world, i.e., a world where tax revenues increase. In a world with interest rates, it is the public finances that are the most prosperous, and it is households that suffer the most. The opposition's argument for tax cuts is legitimate in terms of “rationale,” “justice,” and “love for humanity.” The austerity politicians, bureaucrats, and media who try to block them are being rejected by the will of the people.

(2) How households sacrificed and fiscal capacity increased

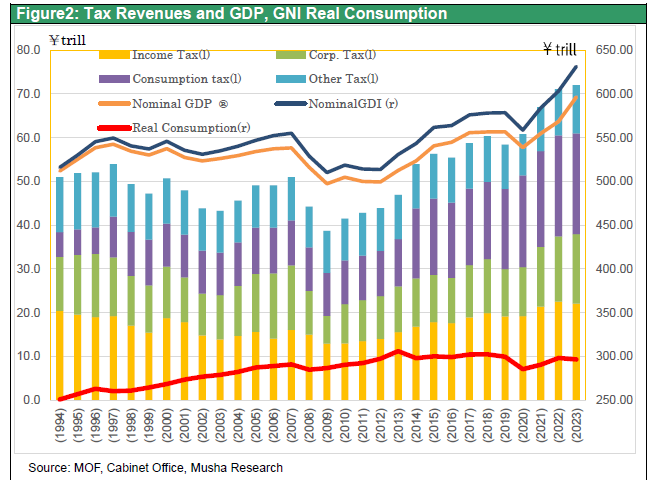

It is quite natural for voters to protest the hardships of life and the heavy tax burden. To date, there has been trivial improvement in the living conditions of the Japanese people. Figure 2 shows that real personal consumption expenditures peaked at 310 trillion yen in the January-March 2014 period, just before the consumption tax hike (5➡8%) in March 2014, and have never exceeded that level in the past 10 years. It began to recover from the ¥272 trillion in the April-June 2020 period during the coronal pandemic, and although it rose at an annualized rate of 4.0% y-o-y in the most recent April-June 2024 period, it remains at a level 4% below the peak of 10 years ago.

Figure 2: Tax Revenues and GDP Real Consumption

Although nominal wages rose slightly during this period, this was eclipsed by a significant increase in the national burden rate (tax and social security contributions) (from 39.8% in FY12 to 46.1% in FY2023), pushing down the standard of living of the Japanese people. During the past 11 years, corporate profits have increased 2.2-fold, stock market capitalization has increased 3.3-fold, and general account tax revenues have increased 1.6-fold, which shows how much the individual has been left behind.

The total income earned by the Japanese people (nominal GNI)in FY 2023 is 647 trillion yen, up 2.7% from 630 trillion yen in the same period of the previous year and up 9.1% from 593 trillion yen in the same period of the two previous years, indicating a sharp and continuous expansion. While real GDP has not grown at all over the past two years at 550 trillion-yen, nominal GNI has been growing rapidly. This is due to the expansion of nominal GDP resulting from rising prices and a substantial increase in the income account surplus from abroad. Since corporate profits, stock prices, and tax revenues are all linked to nominal gross income (GNI), it is only logical that they are doing well.

While households have taken a hit, tax revenues increased 1.6-fold from 43.9 trillion yen in FY2012, just before Abenomics, to 72.1 trillion yen in FY2023, thanks to two consumption tax hikes as well as higher tax revenues from inflation. In addition, an increase in overseas income by corporations boosted corporate tax revenues.

However, the actual state of tax revenue has improved significantly compared to the surface numbers. In FY2023, tax revenue was 72.1 trillion yen, or 1.4%inclease from the previous year's level, which is too small compare with the 4.9% increase in nominal GDP during the same period. The reason for this is that tax refunds and other tax benefits in FY2023 due to changes in the corporate group taxation system pushed down tax revenues.

In FY2024, tax revenues will increase significantly due to the elimination of tax refunds and temporary tax reductions. Tax revenues rose sharply by 25.8% in August 2024, when tax refunds and tax cuts were removed. Tax revenue elasticity, which indicates the percentage change in tax revenue when nominal GDP changes by 1%, was 4.2 in FY2021 and 3.0 in FY2022.Even if we conservatively set at 2, tax revenue in FY2024 can be expected to increase by 8% year-on-year, or a 5-6 trillion yen increase.

The Cabinet Office has estimated that the government's target of returning the primary balance (PB) of the central and local governments to surplus in FY2025 will be achieved for the first time. This assumes a significant improvement in tax revenues.

It is only natural that households, which have been suffering from the triple burden of (1) stagnant wages due to deflation, (2) higher taxes and social insurance contributions, and (3) declining real purchasing power due to inflation, would be supported by a fiscal system with ample tax revenues.

(3) Post-election stock market gains are in sight

Three conditions have come together: the earnest voters' demand for tax cuts, the ample financial authorities' ability to pay, and the LDP's need for the support of the DDP to form a majority, forcing it to accept the tax cut path.

Markets, which plunged a month ago when the Ishiba administration was formed for fear of Abenomics denial and a shift to austerity measures, are likely to have to factor in a deepening of the reflationary policy for a change. Coalition building and the formation of a new cabinet have strengthened the possibility that more reflationary policies than expected will be put in place.

In the U.S., where elections will be held in a week, the post-election outlook is also bright. There are no major blind spots that could trip up the strong U.S. economy. The top priority is to secure employment to avoid social fragmentation, and what is required is a high-pressure economic policy. By maintaining high demand pressure and maintaining a tight labor supply-demand balance, employment and wages must increase and household incomes must be secured. This requires expansionary fiscal policy, rising stock prices, home prices, and other asset prices, and maintaining favorable terms of trade with a strong dollar. Whether it is Trump or Harris, the framework will remain the same. The new industrial revolution is also driving strong corporate earnings. In the U.S. as well, we will see the start of a year-end stock rally as the post-election uncertainty dissipates.